Advanced Wealth Transfer Strategy for Business Owners and High-Net-Worth Families

Introduction

Split dollar life insurance is not a retail product. It is a structuring technique used to share the costs and benefits of a life insurance policy between two parties, most commonly an employer and an executive, or a business owner and a trust. When properly designed, it can serve as a powerful tool for executive retention, estate tax mitigation, liquidity planning, and long-term wealth transfer.

For mid-size and large corporations focused on capital preservation, tax efficiency, and well-designed buy-sell agreements—as is the case with sophisticated advisory platforms—split dollar arrangements can be integrated into a broader risk-management and succession framework. This article provides a deep dive into what split dollar is, how it works, the main structures available, tax considerations, advantages, risks, and strategic use cases.

Insurance?

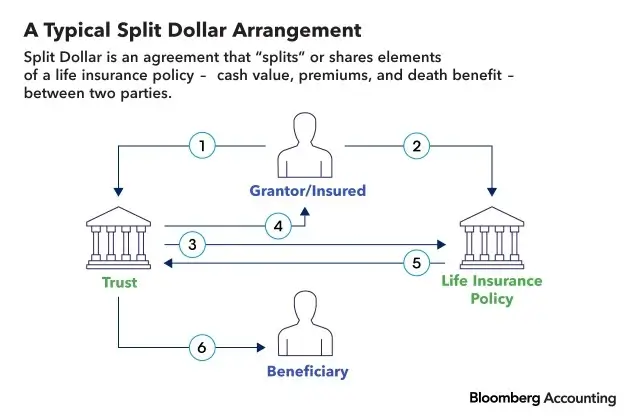

Split dollar is a cost-sharing arrangement involving a permanent life insurance policy. Two parties agree in writing to allocate:

- Premium payments

- Cash value accumulation

- Death benefit proceeds

The term “split dollar” refers to how the economic benefits of the policy are divided—not to a specific type of policy. Most arrangements use permanent life insurance, such as:

- Whole Life Insurance

- Universal Life Insurance

- Indexed Universal Life Insurance

- Variable Universal Life Insurance

The structure is defined through a legal agreement that governs who pays what, who owns the policy, and who receives which portion of the benefits.

Historical Context and Regulatory Framework

Before 2003, split dollar arrangements were commonly structured to maximize tax advantages. However, after IRS scrutiny, new regulations clarified how these plans must be taxed.

The two primary regulatory regimes are:

- Economic Benefit Regime

- Loan Regime

These frameworks determine how premium payments and policy benefits are treated for income and gift tax purposes. Proper legal drafting and actuarial modeling are essential.

What Is Split Dollar Life

Core Structures of Split Dollar

There are two fundamental structural models:

1. Collateral Assignment (Loan Regime)

Under this arrangement:

- The employee or insured owns the policy.

- The employer (or second party) pays premiums.

- Premium payments are treated as a loan.

- The employer receives a collateral assignment equal to the loan balance.

- Upon death or termination, the employer is repaid from death proceeds or policy value.

How It Works

- Employer advances $200,000 in premiums.

- Employee owns the policy.

- Employer records a loan receivable.

- At death, employer recovers $200,000 (plus interest if applicable).

- Remaining death benefit goes to the employee’s beneficiary.

This model is common in executive compensation planning.

2. Endorsement Method (Economic Benefit Regime)

Under this structure:

- Employer owns the policy.

- Employer endorses a portion of the death benefit to the employee’s beneficiary.

- The employee is taxed annually on the economic value of the death protection (measured by IRS tables or carrier rates).

This method is typically used when the employer wants control of the asset while providing a death benefit incentive.

Split Dollar in Executive Compensation

High-level executives are often compensated beyond salary and bonus. Split dollar arrangements can function as:

- A retention tool

- A golden handcuff

- A deferred compensation supplement

- A supplemental retirement income strategy

Unlike traditional qualified plans, split dollar arrangements are non-qualified, meaning they are not subject to ERISA contribution limits. This is critical for executives already maximizing:

- 401(k)

- Defined benefit plans

- Nonqualified deferred compensation

A well-designed split dollar plan can create significant tax-advantaged accumulation while aligning executive and corporate interests.

Split Dollar in Estate Planning

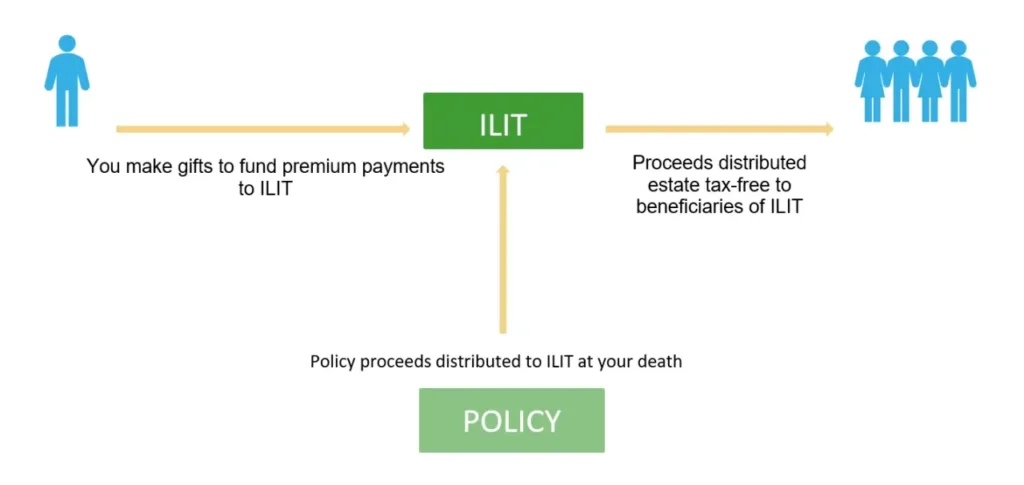

For high-net-worth individuals facing estate tax exposure, split dollar can be paired with an Irrevocable Life Insurance Trust (ILIT).

ILIT + Split Dollar Structure

- The trust owns the life insurance policy.

- The grantor funds premiums via loans.

- The trust repays loans at death.

- Excess death benefit passes estate-tax-free to heirs.

This structure allows liquidity for:

- Estate tax payment

- Equalization among heirs

- Buy-sell funding

- Family business continuity

Tax Considerations

Tax treatment depends entirely on the structure selected.

Under the Loan Regime

- Premium advances are treated as loans.

- Interest must be charged at or above the Applicable Federal Rate (AFR).

- Forgiven interest may trigger income or gift tax.

Under the Economic Benefit Regime

- The employee reports the cost of pure life insurance protection as taxable income.

- The employer may deduct premiums depending on structure and beneficiary design.

Failure to comply with IRS regulations can lead to severe tax consequences. Split dollar must be reviewed by qualified legal and tax counsel.

Advantages of Split Dollar Arrangements

1. Leverage

A relatively modest premium outlay can generate a significant death benefit.

2. Flexibility

Split dollar agreements can be tailored to:

- Vesting schedules

- Performance milestones

- Retirement triggers

- Exit events

3. Executive Retention

Executives may forfeit benefits if they leave early.

4. Estate Liquidity

Provides cash when illiquid estates face tax obligations.

5. Capital Efficiency

Allows corporations to deploy excess cash in a structured risk-management strategy rather than idle reserves.

Risks and Limitations

This is not a simple strategy. Risks include:

- Regulatory complexity

- IRS scrutiny

- Interest rate risk under loan regime

- Policy underperformance

- Liquidity strain if improperly funded

- Accounting implications

Poorly structured plans can become expensive or tax, inefficient.

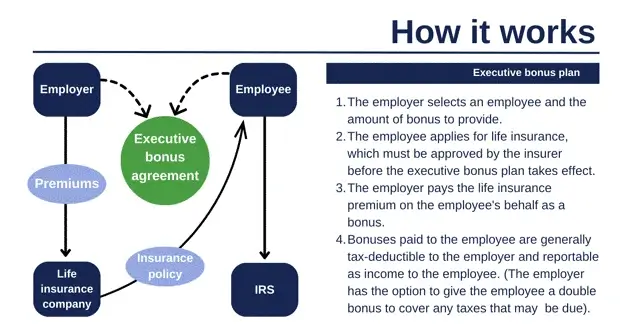

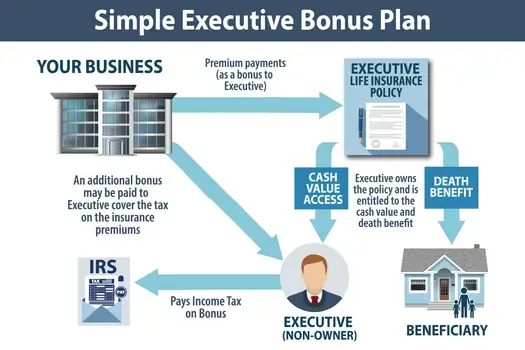

Split Dollar vs. Executive Bonus Plan

Many confuse split dollar with a Section 162 executive bonus plan.

Key differences:

| Feature | Split Dollar | Executive Bonus |

| Policy Owner | Employer or Employee (varies) | Employee |

| Premium Treatment | Loan or Economic Benefit | Bonus income |

| Tax Complexity | High | Moderate |

| Control | Shared | Employee |

| Design Flexibility | Very High | Moderate |

Split dollar offers more customization but requires more advanced planning.

Applications in Buy-Sell Agreements

Business continuity planning often uses life insurance to fund buy-sell agreements. Split dollar can:

- Allocate premium burden strategically

- Preserve working capital

- Structure cross-purchase or entity redemption agreements

It becomes particularly useful when one shareholder cannot personally fund required premiums.

Advanced Use Cases

1. Family Limited Partnerships

Split dollar can be combined with FLPs for valuation discount strategies.

2. Private Equity Executives

Supplemental wealth transfer outside traditional deferred comp limits.

3. Closely Held Corporations

Owner-only split dollar plans for tax-efficient asset repositioning.

4. Real Estate Investors

Provide liquidity where estate value is property-heavy but cash-poor.

Accounting Treatment

Under GAAP:

- Loan regime arrangements are treated as receivables.

- Endorsement arrangements may be treated as corporate assets.

Corporate accounting teams must evaluate balance sheet impact.

Is Split Dollar Still Relevant Today?

Yes—but only in the right hands.

With estate tax exemptions subject to political risk and potential sunset provisions, affluent families are increasingly revisiting advanced insurance planning.

Split dollar remains relevant because:

- It offers leverage.

- It aligns executive incentives.

- It creates structured liquidity.

- It can be adapted to evolving tax environments.

However, it is not appropriate for mass-market clients. It is best suited for:

- Business owners

- Corporate executives

- Families with estate tax exposure

Companies implementing structured retention plans

Implementation Framework

If considering split dollar, the process should follow a disciplined path:

- Clarify objective (retention, estate tax, buy-sell, liquidity).

- Model policy performance conservatively.

- Select appropriate regime (loan vs economic benefit).

- Draft formal legal agreement.

- Integrate with tax counsel.

- Monitor annually.

This is not a “set and forget” strategy.

Common Mistakes

- Using unrealistic policy projections.

- Ignoring interest accrual in loan regime.

- Failing to coordinate with estate planning documents.

- Treating split dollar as a generic life insurance purchase.

- Underestimating compliance burden.

Sophisticated advisory platforms must approach split dollar with actuarial precision and legal rigor.

Strategic Perspective

Split dollar is best viewed not as insurance, but as a balance sheet engineering tool.

For corporations:

It converts surplus liquidity into structured executive retention and future planning leverage.

For high-net-worth individuals:

It shifts estate risk into an actuarially priced, contractually defined vehicle.

For advisory firms:

It represents a high-level planning solution that differentiates from transactional insurance sales.

Final Thoughts

Split dollar life insurance is not a product—it is an advanced structuring mechanism. When executed properly, it can:

- Enhance executive compensation packages

- Solve estate liquidity challenges

- Fund buy-sell agreements

- Align corporate and personal planning goals

When executed poorly, it can generate compliance risk and financial inefficiency.

The strategy demands disciplined underwriting, legal oversight, tax coordination, and ongoing monitoring.

For organizations serving mid-size and large corporations seeking capital preservation, operational efficiency, and long-term succession clarity, split dollar remains a sophisticated planning instrument worth evaluating.

If the objective is leverage, alignment, and structured liquidity—not experimentation—split dollar belongs on the table.